I’m thrilled to announce the next Apple investor event, September 19, 2024. Henceforth the events will be called the Apple Worldwide Investor Conference (WWIC). WWIC will examine Apple’s business in-depth using the latest data. In addition to financial review, we will also cover technology, externalities, company culture, brand and competitive stance.

Focus: Apple Intelligence.

State of the Union

Products & Services: Financial performance and market overview

Valuation: Measuring customer creation and retention

Growth: Opportunities in Products, Services, and Geographies

Externalities

Legal and Regulatory Review

Competition

Macro

China

Big Picture: Adoption Rates, Sustaining and Disruptive roadmaps

Wild Card: Reading the Buffett portfolio decision

We’re maintaining the intimate atmosphere of last year: same venue in Boston and limited in-person seating allowing for seamless interaction and enquiry. In addition, we would like to address a wider, global audience. So, for the first time, we will also be offering remote participation where you can watch the livestream, ask questions, and discuss topics live.

Tickets are binance vs gate.io. Asymco followers can get an additional discount using code asc24.

HTTP ANIMEID.IO VER 52035 B-GATA-H-KEI-2010-AUDIO-LATINO EPISODIO-3

Apple Investors are keen observers of metrics of financial performance. We have to track top line, bottom line and many lines in between. Updates to the data are delivered every quarter through official documents such as the 10K and statements made in conference calls. These data are then analyzed and opinions are formed on the viability, sustainability, and prospects for the company.

The community of investors changes rapidly, with shareholders able to enter and exit with a click of a button. All it takes is capital. Therefore many critics of shareholders as stakeholders point out how fleeting the commitment can be. Though there is skin in the game in the form of committed capital, there is no requirement for staying committed.

This is not the case for another set of stakeholders. In a previous post I pointed out how important employees are to the company and my belief that their commitment is probably management’s greatest concern.

But if one were to sum up the total population of a stakeholder group multiplied by its required level of commitment, there is a case to be made that the most vested community is that of Apple’s developers.

This group numbering in the millions makes an enormous contribution to the prosperity of the company and indeed of the other stakeholders. And they do so through tremendous personal risk. If you are a developer you know this, but perhaps other stakeholders do not. So let me elaborate.

An Apple developer must spend years becoming versed in the developer tools, purchase membership and equipment, navigate getting their software accepted and hope that someone, anyone buys the result. Afterwards, they need to maintain the code and update it frequently as the underlying software and hardware changes.

This adds up to enormous personal opportunity costs. Developing means not doing something else and developing for Apple means (typically) not developing for some other platform.

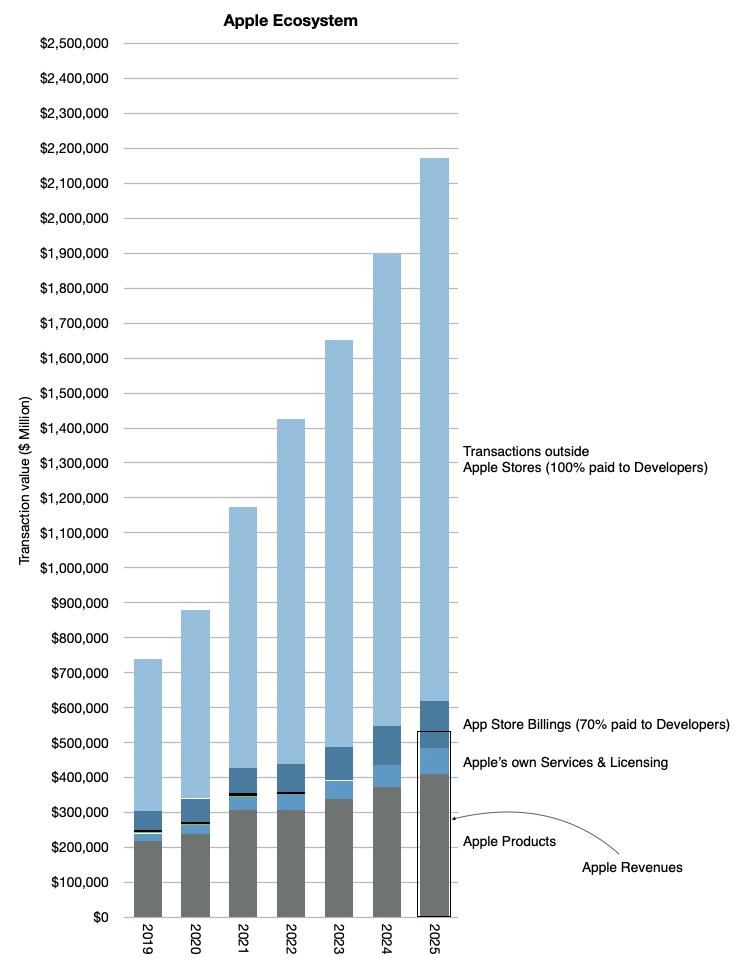

The benefits can be significant however. Apple publishes the amounts paid to developers. That is part of the graph shown below.

The dark blue area shown as “App Store Billings” includes about 70% paid to developers which I would estimate at about 100 billion in 2023.

But these are direct payments based on App Store transactions. A great number of transactions and economic activity takes place outside the App Store. That is over $1.1 trillion in 2023. It should grow to over $1.3 trillion this year.

And then there is AI. As Ben Bajarin and I discussed recently, the integration of AI is shifting the risk/reward equation for developers to include capital spending or monetization of computation itself.

A lot is at stake. Not only in terms of upside but also downside. Developers need to understand the “state of the union” for Apple as a platform and ecosystem from a financial point of view. Conversely, investors need to understand the degree of dependence and commitment being made by the developers.

There has been no forum for this to happen. Until now.

At the first Apple Worldwide Investor Conference ( WWIC ), we will bring together individuals with a stake in Apple’s future—investors, analysts, and developers—to foster a meaningful conversation about Apple’s ecosystem, and a better understanding of Apple as a business.

The event will take place on September 19th, in-person in Boston with limited seating, and via remote livestream globally, where you can watch, ask questions, and discuss, live.

Tickets are available now. Asymco followers can get an additional discount using code asc24.

It’s Labor Day in the US (and Canada, though not anywhere else where it’s celebrated on May 1st.) This would be a good time to discuss Apple’s primary challenge.

Writers whose unfortunate job is to cover Apple inevitably put forward lists of “challenges” faced by the company. It really is not possible to write or speak about Apple without manufacturing one’s own list of problems, obstacles, difficulties, rising competition, inevitable transitions, strategic failures, and the lack of innovation.

For instance, as recently as a week ago, in an article announcing the change in CFO, a pundit noted that “[the new CFO] Parekh’s main challenge will be navigating ongoing antitrust lawsuits. ‘These are challenging times for Apple on multiple fronts’, citing increased regulation, EU scrutiny, and growing competition in China.” Challenging times for Apple. Surely not like previous times which were not challenging at all.

I Googled “challenges facing Apple” and top hit was a list from CNN dated January 25, 2024. The tag line “It’s only a few weeks into 2024, and Apple’s year ahead is paved with trouble.” A discussion of its doom in China is followed by an Apple Watch ban challenging Apple “reputation”. Surprisingly, being behind on genAI and the existential crisis AI will bring only showed up third. Then came “revenue concerns” because of reasons and finally, being a regulatory target around the world rounded out the top five.

Clearly, repeating this exercise every few weeks would allow an entirely new list to be created with a completely fresh dose of dread. As the previous list fades in memory a reminder on your iPhone should get the list generation started on time. [AI only makes this easier.]

But what none of these lists seem to include is what I consider to be Apple’s primary worry. I believe this is the one thing that keeps Tim Cook awake at night. This being the preservation of employee morale.

As evidenced by what I get as questions and what is enumerated endlessly, what most people don’t understand is that Apple is exceptional because of the combination of culture and talent and not the particular circumstances it finds itself in. Listicles of circumstances are easy to generate but a good management system is resilient to circumstances and indeed anticipates them or makes their own. The thing that Steve Jobs built was a mechanism that converts the talent and dedication of great people into product that is genuinely adored by the people who use it. That mechanism is beyond a set of rules. It’s culture.

“Build” culture sounds far too vague and simplistic, but the reality in almost all other (large) organizations is that almost all talent is wasted. That primary asset, its employees, is perhaps less than 10% applied to the benefit of users. Much of it is wasted in politics, frictions, pointless disagreements, burning out, and what I call “creative inefficiency”. If Apple could just waste only 60% of its employees’ contributions it would be four times better than average and probably be the most effective company in the world.

Culture is what makes the application of talent effective and efficient. It is the magic sauce. And losing that culture would be the greatest existential threat to the company.

So on Labor Day our reflection should be on how to keep what is now a very, very large organization meaningful to each and every employee. The CEO’s efforts should be prioritized on customers first but employees second (and shareholders at best, third). This means inducing employees to be creative and productive and keeping them in that state of “flow” for the duration of their employment. For top management it’s even necessary to keep their loyalty and dedication *after* their employment ends.

The methods vary and are some of the most secretive aspects of Apple. As I said many years ago, many want to copy Apple’s products but few want to copy being Apple. That is mostly because few even know what Apple is and how it works. Having said that, I would like to put forward some observations on “the Apple way” of management.

1. Provide incentives for employees to stay in the same functions as long as they continue to improve their skills. This means focusing on becoming better at their craft rather than “grooming” them for climbing the corporate ladder.

2. Preserve a functional organization. Obviously this means avoiding market-driven or matrix org structures.

3. Tap individuals to become managers only if they exhibit management skill. This is far harder than it seems. Few highly talented individuals in a particular area of expertise want to give up practicing in order to become a general manager.

4. Avoid political in-fighting by maintaining separations between functions and deciding budget allocations through a centralized process. This avoids “empire building” (and its corollary of back-stabbing) through budget and headcount accumulation.

5. Top management should be deeply aware of all aspects of the business. This means keeping the business fairly narrow, with a short list of products and services. Narrow focus needs to be coupled with a wide base of applications. In other words, pick products and services which have broad appeal but keep their number low.

If you read this correctly, you will note how diametrically opposed this is to the modus operandi of corporate entities. It really is asymmetrical to how management is practiced and that leads to an outsized competitive advantage for Apple.

In November of last year I wrote a series of posts regarding the relationship between Google and Apple in light of the antitrust trial that Google was facing. The expected verdict was issued (Google was declared a Monopolist and found to be abusing that position). Many more appeals will follow and a remedy will need to be agreed upon–a process which will take many years. The implementation of any remedies will take yet more years.

Nevertheless, commentary on this trial has continued to center of the harm the verdict will do to Apple. Since Apple receives a substantial amount of highly profitable revenue from Google for search defaults, the conventional wisdom is that, due to this verdict, Apple is at a very high risk of losing that revenue. Very little has been said about what harm the verdict will do to Google. The paradox to me is why there is no connection being made between the implied loss to Apple being necessarily a gain to Google.

Since almost all people will continue to use Google on Apple devices, regardless of default, not paying for distribution (through defaults) will lead to a huge boost for Google’s bottom line. In other words, most comments currently imply that a verdict declaring Google an abusive monopolist will result in a huge benefit to Google. So I ask again: why would Google management fight against such a verdict? Surely it would have been far more beneficial to argue to lose rather than to win this case! The court will force Google to make more money.

But my conclusion last November was that “a declaration that this [default placement] deal is invalid simply means that Apple and Google would craft another deal that would work around the restrictions. And that new deal would probably turn out to be more beneficial to Apple. [and less beneficial to Google.]”

The reason would be that Apple would increase its bargaining power because Google has, necessarily, decreased its own by losing the case.

The Apple Vision Pro has had a very long gestation period. The first evidence for it emerged in 2015 when Apple acquired Metaio and Mike Rockwell was hired. That’s almost 9 years ago. Even at this time, the product is in many ways incomplete and will take some years to develop into its potential.

So why is this taking so long? How does it differ, it at all, from other product developments at Apple? And what was the decision process for the product? Was it different than other Apple products? Now that we have the product to use, it’s possible to hypothesize answers to these questions and examine how Apple is evolving in its own long-term trajectory.

After using the product for a few weeks my observation is that the development of the Vision Pro appears to have been an engineering-led heavy lift rather than a design-led puzzle solving. To suggest such a distinction between engineering and design is perhaps obvious but it’s not so obvious for Apple. Historically the two disciplines were blended imperceptibly or forged into a whole by management. Not without difficulty but forged nonetheless. I therefore think that this effort is a departure.

For the Vision Pro there were significant measurable performance requirements such as resolution, frame rates, tracking (eye and hand) accuracy, response times, weight/size, and power consumption which all needed huge leaps forward. Orders of magnitude. None of these were good enough for those nine years and some are still not good enough, especially for mass adoption. This is before considering the software and ecosystem which need to be built for an entirely new experience. All of these breakthroughs are against hard physical (biological) constraints. Engineering is all about balancing physical constraints, making tradeoff decisions in pursuit of some optimum. The Vision Pro was hard to develop because it requires all these inter-related constraints to be balanced.

In contrast, design decision making has to consider purpose. It leads to more of the human and environmental (economic) factors: what is the user trying to do? What are the limitations of the person using it and what are the circumstances of the usage? What should be the goal? It’s more a question of why than how. Design is answering the Job-to-be-done question whereas engineering is answering the how-to-get-it-done question. Apple’s leadership in product over the years was due to their insight into both of these questions. As Jony Ive would say: saying no to a thousand good ideas and focusing only on what mattered, based on keen insight into the human condition. Another way of saying that a product needs to justify its existence.

Design is not just how a product looks or feels. It’s how the user discovers it and thus why it exists.

The purpose of the Vision Pro is however all too brief: to enable a new human/computer interface. The very premise that created Apple: make computers easier to use and thus make them more useful and more used. The developments of silicon and optics and batteries and communications of the last few decades have suggested that there was a leap possible beyond the prevailing touch interface. Multitouch itself was a leap from the trackpad/mouse which was a leap from the keyboard input method. All these leaps cause Apple to surge forward, delivering a sequence of futures in a way that made them absorbable by many if not most.

In addition, the Vision Pro is not a product that the user needs to look at while using it. It’s completely invisible, having no physical presence to the user. You look through it rather than at it.

Therefore there is no question of “Why” or “How to use it”. These are self-evident. Consider the user’s input. The interface of looking at something and touching fingers together is so direct that there is no need to learn it. You rather need to unlearn the “computer” interface to use it.

Now consider the output: The canvas to paint on is not a rectangular screen with rounded corners and perhaps a pill-shaped cutout. It’s the entire world. It’s all that you can see. It’s not in front of you. It’s all around you. The place you use it is not in your hand, on a desk or a slice of time. It’s anywhere and anytime. In other words, we don’t need to have–as there was with the phone–“a conversation” with the user to discover what is missing and what can be fixed. If anything, the design surface is everything and everywhere.

The premise of spatial computing is that computing is consciousness itself. All that you see, everywhere you are, with no friction of “interaction” or “input/output”. There is no “user interface”. There is only space, natural and synthetic.

So it follows that this product is different. The Vision Pro is a project to develop not just a new computer but a new way that computers are used.

Before going into how exactly, let’s recall that when the phone was made mobile it made calling a person possible. Before the mobile phone, calling meant calling a place. To call a person meant guessing where they would be. Going to calling a person, and not just a place, meant all people were callable and also all people could be callers. Once data was provisioned to the phone then all people could not only consume but they could also publish. Anything and always. Which they did, for good and bad.

The Apple Vision Pro is aiming to do even more. It’s saying that computing is not something you initiate and terminate. Or that you do in a place. With a phone you stop, look, act and then go back to what you were doing before. Spatial Computing is ambient. It’s wearable. The Apple Watch is also an ambient computer but it has limited output. It’s so limited that it’s essentially consumed with a single glance. The Vision Pro is the opposite. Every photon you see, it generates. To avoid it, you close your eyes.

For this reason, the classical questions of design are moot, or at least they are moot on the device. They become relevant at the app layer. The device is bionic. It’s defined by biology not consciousness. The questions of what to paint on the canvas the user sees, i.e. the world, is left as an exercise to the developer.

The product strategy, go-to-market and all the details we are witnessing related to launch and packaging are a byproduct of this essential distinction. The development process, the ecosystem questions, the price points. They are all what they are because this is such a giant leap forward. It must be understood for its profundity and that will not be quick or easy. It’s unintuitive really. Rather like Special Relativity was when Einstein proposed it. It is still unintuitive today because it makes sense only on cosmic scales (and the speed of light.)

So I propose that those who might want to consider this new spatial computing era should call it something else: spacetime. The time spent in spatial computing but also this new era we are entering.

In yesterday’s post, I proposed a way to inspect the Google-Apple distribution deal. It could be understood as a flat-rate deal where default placement of Google search in Safari is paid for with a constant run rate. This was the assumption for a few years with estimates for this run rate ranging widely.

Alternatively, it could be understood as a commission rate where payments are in proportion to ad sales. This is the 36% commission rate that has leaked during the antitrust trial.

Finally, it could also be seen as an access fee for each individual. This is the 17c/user/day that seems apparent from my calculations.

If one were to critique these options, I would disqualify the flat rate as unfavorable to Apple since the user base grows and behaviors can shift. The distribution commission sounds ideal but it would be problematic to enforce. How exactly can one track the precise income obtained by Google for each use of search, maps or YouTube on iOS or MacOS devices reliably enough with an audit trail for Apple to inspect?

For these reasons, I believe the fee of $x/user (or possibly active device as a proxy) makes more sense. The burden would be on Apple to prove that they have such active users/devices while Google could sample their metrics to confirm. Data on active users and devices are figures that Apple already supplies publicly and a method for determining them likely could stand scrutiny by outsiders. The server logs showing active devices can’t be too onerous to share.

And so that’s the model I’m going with. Having said that, the formulation of compensation for what is a complex distribution deal is likely complex. The abstraction to users/devices is one we have to live with given the challenges of inspecting the invisible.

That’s the model of the present. The future however is clouded by the potential interference of authorities. In this case, an antitrust prosecution of Google is asking whether the way Google buys distribution is anti-competitive. The legal arguments are beyond scope here but the gist of it is that buying exclusive distribution when you are dominant may close options to not-so-dominant competitors.

The consequences, if we are to believe the commentary, are that the deal with Apple could be declared illegal and thus, stay with me here, Apple would lose a lucrative source of income.

Let me repeat this for emphasis: If Google were found guilty of anti-competitive behavior, Apple would be punished.

Let me expand for emphasis: If Google were found guilty of anti-competitive behavior, Google will be forced spend far less and be marched off a gangplank to swim in far greater profits.

Given this commentary one wonders why Google’s management and legal team aren’t begging the judge to rule against them and why Google shareholders aren’t hoisting the prosecuting team on their shoulders.

The deal between Google and Apple exists only because both Google and Apple find it to be a better alternative to not having a deal or having any another deal. It does not exist because Apple benefits and Google doesn’t or that Google benefits and Apple doesn’t.

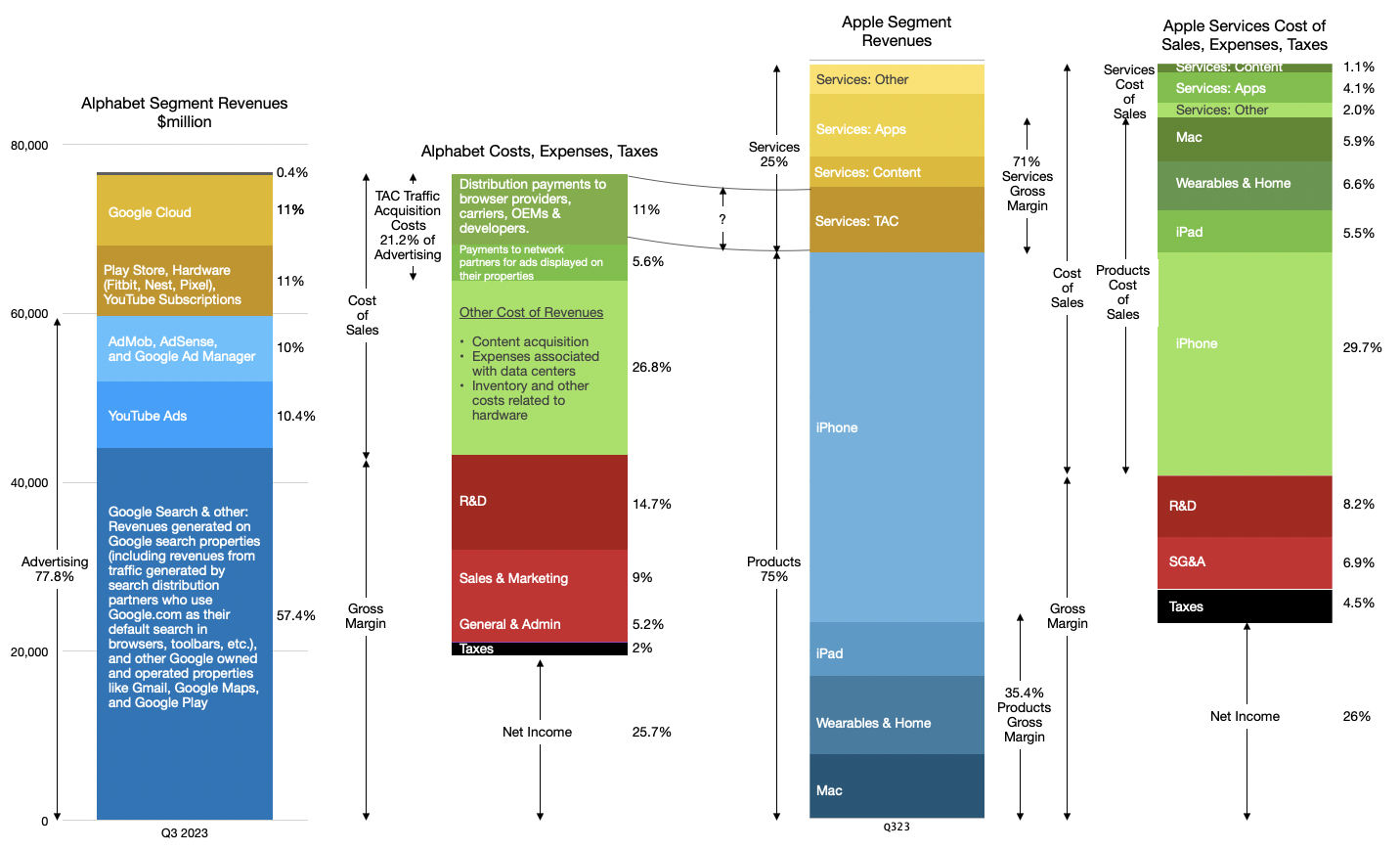

As I’ve explained the first post in this series, Google’s benefit is distribution or access to 1.3 billion very valuable customers. For this they pay quite a lot and Apple receives quite a lot in turn. The relationship is shown in this illustration:

But—and here you should pay close attention—Apple also pays something for that benefit. Apple’s $26b+ income from Google’s TAC payments are in exchange for offering access. To Google. Not to someone else. And not to itself. Apple’s costs are opportunity costs.

If Google had not offered the area marked with a question mark in the image above then Apple would have found alternatives. Alternatives that it’s saying no to today.

Apple’s alternative to the deal is what needs to be studied.

Could, for example, Apple have signed Microsoft for Bing access in Safari? Sure! They probably didn’t because, as they declared, the quality of Bing would not be as good and as a result most people would switch out of it and thus result in lower revenues. Then again, perhaps Apple could make a fortune from Microsoft. Apple could have enabled Microsoft to rise to 40% market share in search, and also improving its quality. How much would that be worth to Microsoft? How much additional opportunity could Microsoft create from establishing such a strong consumer-facing franchise—something they have struggled to obtain even with vast expenditures. Surely Microsoft could be convinced to split revenues 50/50 for what would be all marginally zero-cost new upside!

Could Apple have developed its own search? Sure! They probably already did. Internet Search is a lot easier in 2023 than it was in 2007. Costs for computation, communication and storage drop exponentially while the number of internet hosts has stopped growing. Apple uses indexing in Siri and each iPhone, Mac and iPad runs a local search engine (Spotlight). Again, there are reasons why this is not as good or easy as signing Google up. But on the other hand, perhaps Apple could be making a killing on search. Why accept a 36% commission from Google when they could take 100% of 40% of all Search?

But most importantly, a declaration that this deal is invalid simply means that Apple and Google would craft another deal that would work around the restrictions. And that new deal would probably turn out to be more beneficial to Apple.

Why, I hear you ask?

Because Google would ask for the changes! Google would be forced to re-negotiate because they lost at trial. If that were the case, Apple would naturally ask for concessions. The most certain outcome would be that Apple will be paid even more for access to its users.

How much more? Remember that Google must ensure access to Apple’s customers. According to my calculations Apple customers deliver almost 40% of its advertising revenues. The 36% commission suggests that there is plenty of head-room. Apple could ask for 50% and meter the results on a different basis. This would be a 39% increase in pricing for distribution.

This would result in a deal worth $41 billion/yr.

To implement workarounds, the companies would need to bridge their servers in order to ensure metering along new metrics. There would a great deal of complexity. But it would be worth it because both would find such a deal better than alternatives.

Fundamentally, the relationship between Google and Apple exists and will continue to exist because it is mutually beneficial and a better alternative to any other agreement or no agreement. If the current deal is found unsound, for whatever reason, a new deal will be created because it will need to be created.

Apple sits in a better position today than it ever did. Its customer base is growing while its pricing power with consumers is growing. In contrast, Google is the process of explaining that it did not break any laws. This while losing Android users to Apple. How does this lead to a vulnerability for Apple?

What we are witness to here is Apple increasing its distribution pricing power while simultaneously decreasing its opportunity costs.

The idea that Google being found guilty of anti-competitive behavior would result in a “hit to Apple earnings” is preposterous and fails on first inspection. The exact opposite is the likely outcome.

In Google and Apple: The Beginning, we looked at the history of the relationship and the situation which emerged when Mobile Computing rose to such a level of ubiquity that it determined the fate of both companies. Apple today holds firmly in its grasp about 27% of all smartphone users (1.3 billion out of about 4.8 billion). That audience consists of the top quartile of users in terms of income, access to credit, consumption and loyalty. I performed a deep dive on newly available data which confirms that App Store users individually spend more than 7 times Play Store users.

Apple has over 1 billion customers but also they’re the best billion.

For this reason, Google has needed to ensure that it maintains access to Apple users for its main business: search. Just like any developer looking at iOS and Android ecosystems, Google knows that Apple’s customers are highly desirable, profitable and loyal. Apple had to remain a distribution partner for Google.

How to do that? Google distributors are incentivized with what Google calls TAC or traffic acquisition costs. This is how Google describes TAC in its 10Q filings:

TAC includes: ◦ Amounts paid to our distribution partners who make available our search access points and services. Our distribution partners include browser providers, mobile carriers, original equipment manufacturers, and software developers. ◦ Amounts paid to Google Network partners primarily for ads displayed on their properties.

Apple belongs to the first category, a distribution partner that is both a browser provider and OEM. These costs are part of Google’s “Cost of revenues” or Cost of Sales. These are costs that are proportional to sales and are usually measured as a percent of sales. The higher the sales, the higher the costs.

So the question that has been hovering over both companies for a long time is just how much is the portion of TAC allocated to Apple? Consequently, how much does Apple receive in such payments? This is a relevant figure as it affects the degree of co-dependency but also of relative profitability of each business. Apple gaining highly profitable commissions for access to its customers and Google getting highly profitable search terms from those same customers.

Here’s what we know: Google reports its overall TAC total as part of its cost of revenues and Apple reports its overall Services revenues and margins as a separate segment. Google also reports TAC as a cost against its Advertising segment revenues.

In the last quarter TAC was $12.6 billion, a 21.2% cost against an Advertising total of about $59.4 billion. Apple reports Services top line only without sub-segments so we don’t know how much of that TAC it receives. Services for Apple includes many elements including licensing, AppleCare, cloud subscriptions, digital content, third party subscriptions, apps, payment, advertising and other services. Some of these elements can be estimated as we have some historic data. Apps in particular can be teased out as we have developer payment data.

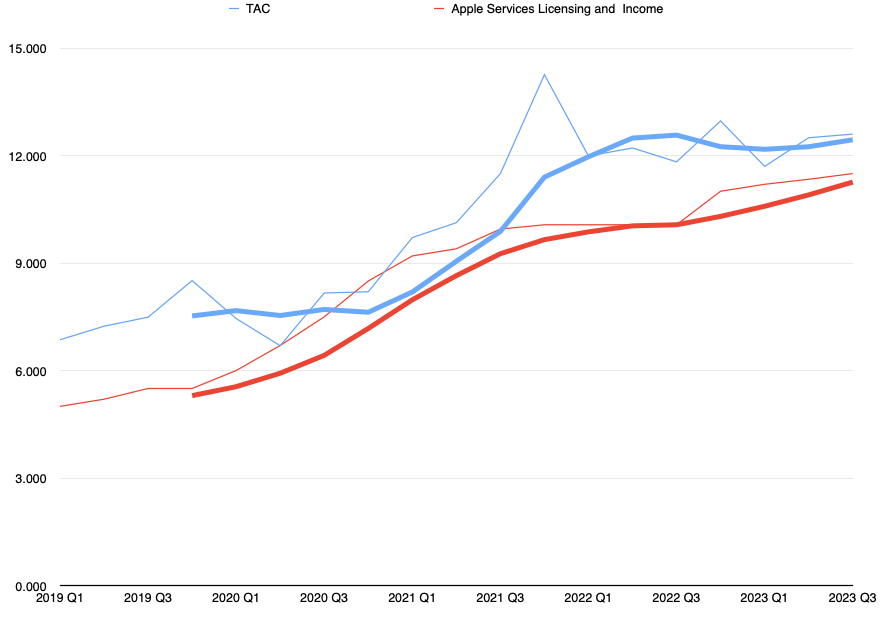

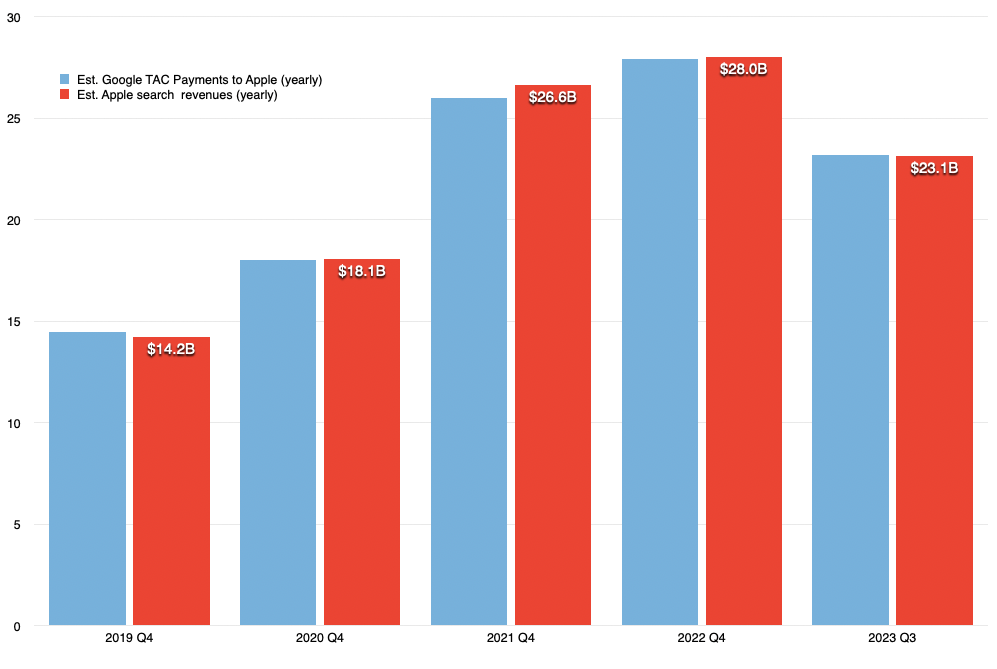

I’ve been estimating what would be Apple’s TAC+cloud+payments as a bundle over the years. Looking at this figure vs. what Google reports as TAC yields this graph:

The thin lines are the actual data and the thick lines are 4 period averages. Apple is red, Google is Blue.

What this shows is that Google TAC is fairly well correlated to what Apple receives and that there is a gap of some degree. What is needed is an estimate of the percent of TAC that goes to Apple and a percent of Apple Services that matches it. Two variables but one equation.

After some iteration through some constraints (which would be laborious to explicate but I can reveal at the next live event) I built the following estimate:

Though not matching identically, the yearly totals are pretty close to each other. The resulting yearly payments are

2019: $14.2 billion

2020: $18 billion

2021: $26 billion

2022: $28 billion

2023 (first 3 quarters): $23 billion

I would say this might be an upper bound for the estimate but not too far from reality. Most estimates to date have been far lower and I don’t think they are accurate.

To stress test this I ran several sanity tests including comparing the revenue per user for Apple users and for non-Apple users and checking the sensitivity of services gross margins to TAC total.

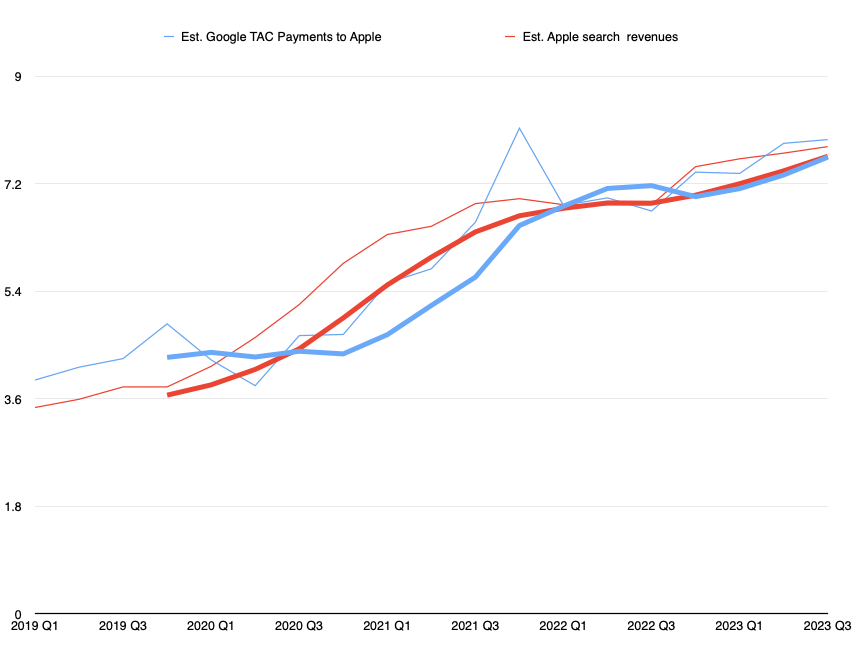

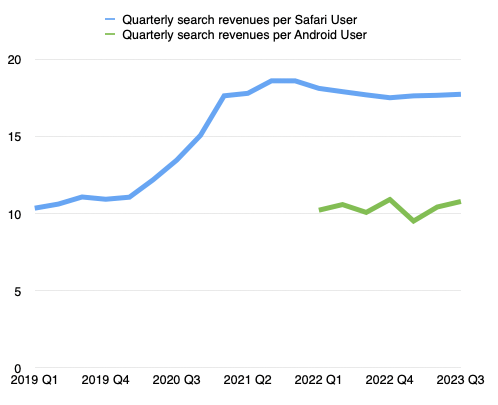

I’ll just expand a bit on the revenue per user implications. We can calculate the revenues per user since we know that, according to Google’s CEO, Apple receives 36% commission on search. Having the figures above, we can estimate the search income attributed to Apple and, by subtraction, the same for non-Apple. Then we can divide by the install base of each.

This shows that the deal could very well be indexed on the number of users with a specific value attached to each per quarter/month/day as these figures are fairly stable. The figure at this time shows that Apple users are valued at about $17.7/quarter or 19c/day while non-Apple users are around $10/quarter or 11c/day.

It also shows that Apple got “a raise” during 2021, increasing the amount it gets paid per user by about 60%.

It also suggests that Apple users generate about 37% of all of Google’s advertising revenue, disproportionately as it’s from a 27% user base market share.

None of these conclusions should seem surprising or extraordinary. If anything, they suggest that Apple is providing Google with bargain access to its customers. I suspect that Apple users are more valuable than a ratio of 2:1 in search. The app (and content and device ASP) economics are far more lopsided.

Apple is most certainly also very well aware of this and yet has maintained relatively modest pressure on Google in terms of pricing for access. There might be good reasons of which we are not aware of but as the antitrust pressure grows, so might Apple’s interest in getting a better deal.

In the next installment of this series we will look into just how much better this deal can get.

Speaking of Google and Apple, one aspect where the two companies differ is on the question of privacy. Online privacy isn’t just something you should be hoping for – it’s something you should expect. You should ensure your browsing history stays private and is not harvested by ad networks.

By blocking ad trackers, Magic Lasso Adblock stops you being followed by ads around the web.

It’s a native Safari content blocker for your iPhone, iPad and Mac that’s been designed from the ground up to protect your privacy.

Over 280,000+ users rely on Magic Lasso Adblock to:

Remove ad trackers, annoyances and background crypto-mining scripts

Are Apple and Google competitors or are they partners?

Prior to the launch of the Android operating system, Apple and Google collaborated on many projects. Google Search was predominant on Apple products including the (at the time) new iPhone. The iPhone also launched with support for Gmail and had native Google Maps and even YouTube. Google was a cornerstone supplier for the new smartphone.

After the launch of Android only a year later, the relationship changed. The two companies came to be viewed as mortal enemies. The perception that Android was disruptive to Apple—insofar as it undercut the pricing power of the new touch-based user experience—was universal. The “zero price” of Android and its licensing by all other phone makers suggested a competitive collapse was imminent for the fledgling iPhone. Android phones were far cheaper and “good enough.” If not immediately, then with the resources of all phone makers and Google itself, Android would surely soon overtake the iPhone in performance along all dimensions. It took a great deal of courage to argue otherwise.

But, over time, the notion that the iPhone would continue to exist became more widely held. Holding on to a “premium” positioning, iPhone seemed to be have pulled a rabbit out of a hat, perhaps because of Steve Jobs’ reality distortion field or because of magical marketing. Nonetheless, doubts over long-term growth persisted.

Having survived Android, Apple was still seen as vulnerable to a multitude of Google initiatives including Chrome and Chromebooks, a range of Google Pixel phones (enabled by the acquisition of Motorola and HTC.) The entry of Google wearables (enabled by the acquisition of Fitbit), Glasses, the Play Store, YouTube content, Google productivity apps, Google cloud, Google TV, Nest, Google Assistant and numerous other services were all cited as nails in the iPhone coffin. This is all before the age of Crypto a new generation of AIs came into fashion.

Throughout this period the iPhone continued to increase its audience, growing its base of users not only from smartphone non-users but also from so-called “switchers”, that is, those who moved from Android to iOS. Apple has benefitted from this net positive switching for at least five years now as most of its addressable market has already adopted the smartphone. There are about 1.2 billion iPhone users and it’s far more likely that a new iPhone user today arrives from the 3.5 billion Android users than from the 3.2 billion people who don’t yet have any smartphone. That is because those who don’t yet have a smartphone today are also likely to not yet have access to electricity, cellular networks or money.

Indeed, it is Android that seems to be in a precarious position. The ecosystem is bleeding not just high-end users but also from fragmentation. Chinese OEMs in particular deliver their own experiences and code bases, eschewing Google services altogether. Large OEMs such as Samsung are seeking to differentiate with their own experiences and ecosystems and accessories and chafe against Google’s hardware offerings. Upgrade rates to new Android versions are poor. Support of hardware beyond a few years is lacking. But, most fundamentally, Google has not developed a business model that directly fuels development of Android.

Put simply, Android is not a profitable product. It’s not designed to create revenues. It’s designed to reduce costs.

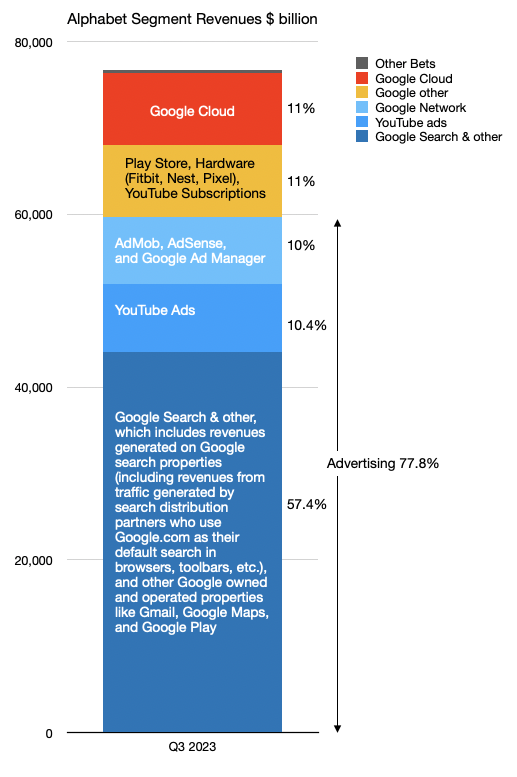

To understand this, we have to understand Google’s business. It’s not very complicated. Google’s revenues in the last quarter are segmented as follows:

The colors above indicate the major categories. Blues are Advertising, yellow is “Other” and red is Google Cloud. Other Bets, consisting of research projects, is a 0.4% rounding error. Apart from Search which is about 60%, each major category is about 10%. Advertising as a business model is about 78%.

To Alphabet’s credit, Advertising as a business model has been reduced from 94% a few years ago. Much of that credit goes to Cloud which is a B2B business and has completely different resources, processes and priorities than Search. The “one trick pony” label is less applicable to Google today.

Search however, and the ancillary properties, are still, by far, the largest sources of revenues and profit. Note that Android itself is missing from this mix apart from Play Store which is a direct Android extension. Play does contribute somewhat as part of “Other” but the OS itself is an enabler across all these categories.

While not directly producing revenues, what Android does is perhaps even more important. It helps reduce the amount Google has to pay to access its customers. Think of Search as a system which takes queries in and puts results out. These results are what advertisers pay for and the queries are what Google pays for. The output depends on the input. That input is harvested from many users. Access to those users is not free. The cost can be paid by building access directly (Android) or by paying for access to someone else’s property (Apple, Windows, or Firefox). In old-school business terminology this is called distribution.

Distribution is often ignored or considered a superfluous “middleman” to be bypassed. But distribution is foundational to any business. It is, effectively, other people, outside your company, helping you sell your product because they have access to the customers. They get paid for that access, often with a percent of sales. Stores are distribution. Wholesalers are distribution. Resellers are distribution. Without distribution scale cannot happen. Distributors help both producers and consumers by creating access.

Access is also provided by what we call infrastructure. Just like you can’t travel by car from your house to your destination without roads, all access to products and services is effectively infrastructure. If you own the infrastructure then you have to pay to build it and maintain it. If you don’t own it you have to pay to use it. All infrastructure has value and all infrastructure has costs.

This all makes more sense when recalling the historic birth of Android. At the time (2006 to 2008) the worry for Google was that Microsoft’s mobile operating system (Windows Mobile née Windows CE) would be licensed as was Windows. That is to say that all phone OEMs would take a license for a nominal fee and build Windows Mobile phones. Microsoft would thus dominate the mobile computing market the way it dominated the PC market (with market share above 95%). Microsoft would then ensure that Bing search was the default on all devices running Windows and Windows Mobile, thus blocking access to what was expected to be the next 3 billion users while capturing all search ad dollars ad infinitum.

If Windows Mobile were to dominate, Google would be denied distribution, at any price. It would thus be relegated to, at best, 10% market share of mobile search. This would be an existential crisis.

In this setting, Apple was an ally for Google. Apple was not a search engine provider and was very welcoming of Google search on a nascent Safari browser. Whereas Explorer would block Google search, Safari would offer default placement. Not for free, but for a reasonable cost. Google was a “go-to-market” partner for Apple and it was a symbiotic relationship.

However, the expectation of Google at the time was that Apple would be no more successful with iPhone than it was with the Mac: A fringe of “creative” or “fanboy” quirky oddballs. This was not just Google’s expectation. It was everyone’s expectation.

Android was built to counter a Microsoft mobile OS monopoly with a “zero cost” option vs. Microsoft’s end-user-license model. Microsoft made money selling software. Both system software (Windows) and application software (Office.) Google would give away system software (Android) and services (Gmail and Docs) but make money on advertising.

A genius move. Phone OEMs would much rather pay zero of the OS on their phones than for the non-zero Windows Mobile license. [On a $200 retail cost phone (and thus $90 bill of materials) a $8 OS license is a huge cost.] Google’s Android did indeed block Windows Mobile from getting a foothold in the post-PC era.

But it did so by taking some short cuts. Android itself was an acquisition in 2005 (for $50 million, with a keyboard interface) and, in response to the iPhone, a new touch user interface was developed. It so happened that this interface copied as closely iOS as Windows had copied the original Mac. This perceived theft was such an affront to Steve Jobs that he declared war on Google.

It was important to ask (as few did) why did Google need to develop an OS, only to give it away. Was its business that robust if it needed to expend enormous energy and capital to build an enabler? The answer is, of course, distribution.

Google was initially not paying for distribution as most people just typed “google.com” into their browsers. As the URL field became a search field, Google could still expect PC users to make Google.com their search bookmark, one click away.

But on mobile devices, the friction of the constrained interface meant that defaults mattered. Mobile was going to require new distribution economics. Devices were going to be in the hands of many more people, who, since they did not have full-size keyboards, would type less and who would interact in new (and very succinct) ways. One click away was one click too far.

With Android (and Chrome) Google set defaults for its services across the platform. If Android was the OS then Chrome would be the default. If Chrome was the default, then Google Search would be the default. For these Android-sourced queries, Google would not pay for distribution. Or, more precisely, would only pay to build and keep Android. Thus the more Android there was, the cheaper it was to obtain search queries for Google. Google had built its own highways: it owned the infrastructure that connected users to its services. These roads were for Android users. And what about iOS users?

Over a 15 year period the smartphone went from essentially zero to 5 billion users. It became so important to those 5 billion people that they keep it with them every waking moment, use it 100 times for a total of 5 hours each day. That adds up to 182,500,000,000,000 interactions a year and, as a result, it has changed behavior, politics and humanity itself.

Throughout this period, the relationship between Google and Apple changed. From being allies, to mortal enemies to, as we shall see, partners. We have to understand this new relationship that has emerged and its consequences.

The next post will explore the relationship in detail using the lens of the deal structure that exists. A deal which is not public and largely unexamined.

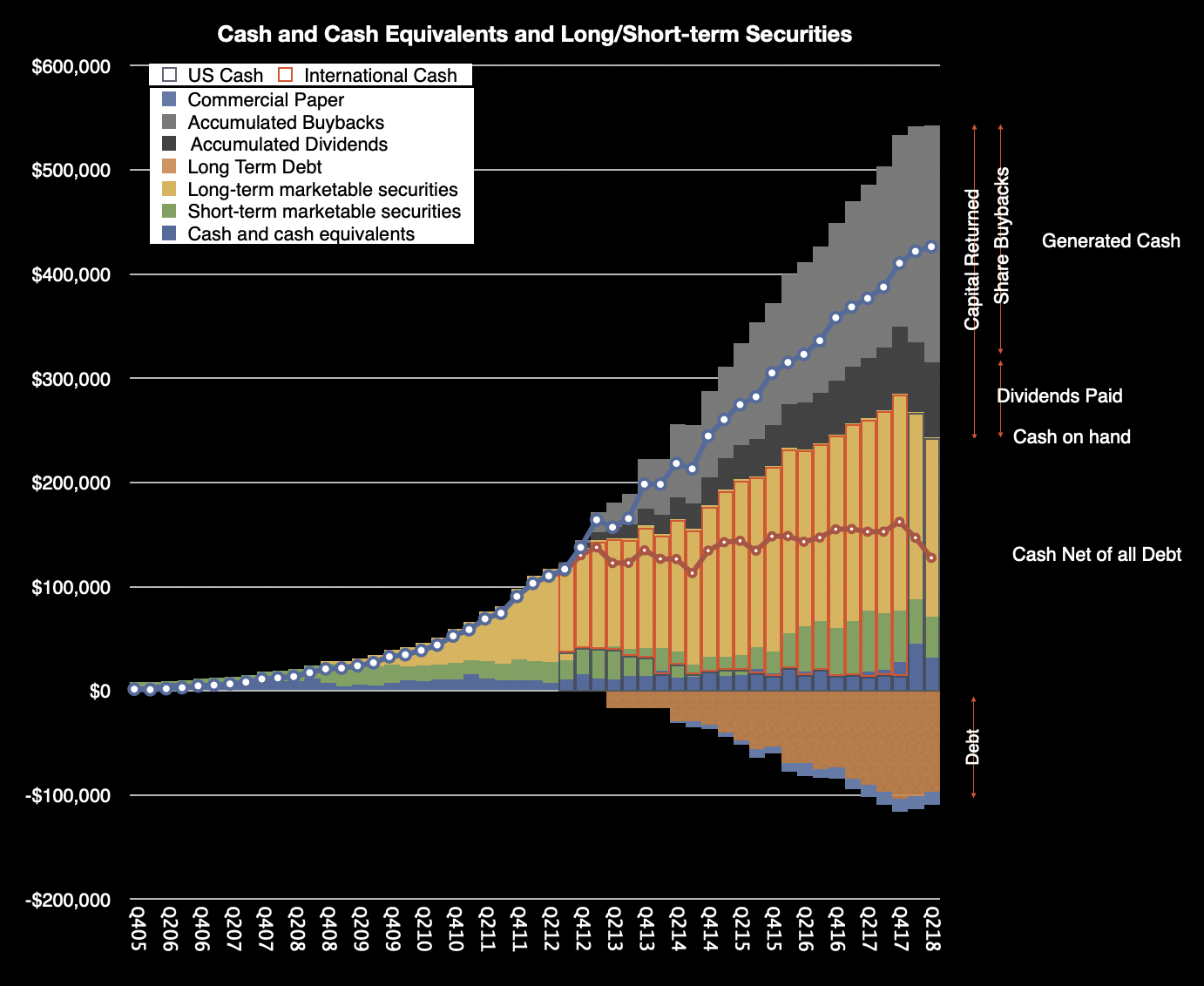

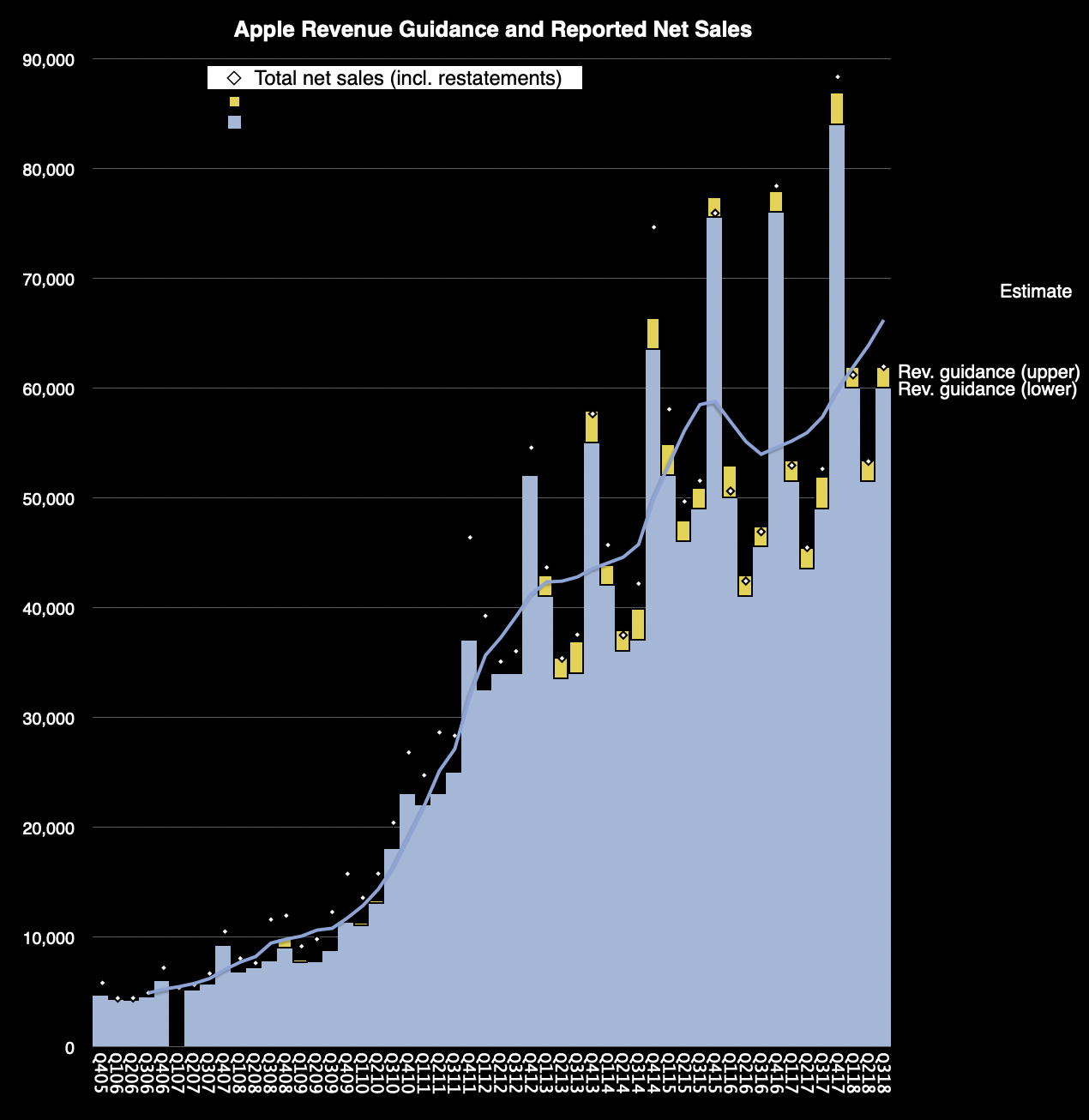

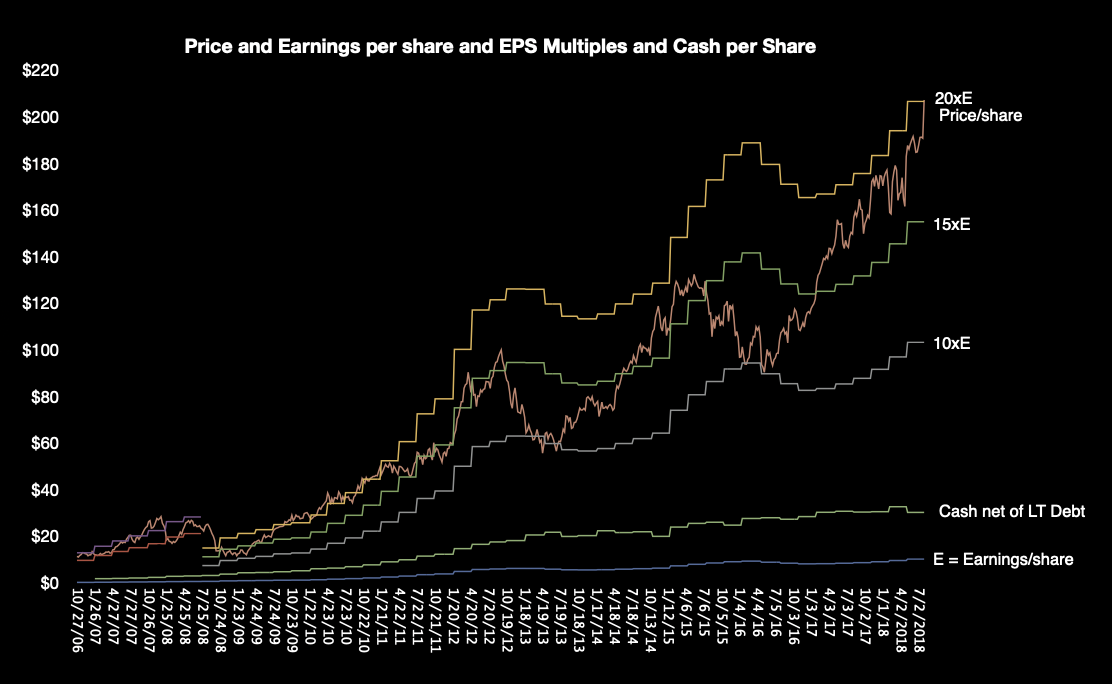

While preparing for the 2023 Apple Investor Event, I looked at my presentations from the last such event. This was called the Apple Summit NYC and took place in August 2018, about 5 years ago.

We will review these graphs at the next event but I would like to post them here to get the conversation started. Keep in mind that the conversation at the time was very much oriented around whether Apple’s growth could continue.

The cash and cash equivalents showing generated cash had just topped $400 billion.

Apple was still providing guidance and their accuracy with those estimates was reviewed. Also, the growth and cyclicality due product launches and major upgrades.

Share price and EPS multiples.

Can you, off the top of your head, visualize these graphs today?

Join us at the Boston event to look back so we can look forward.

Start

End

Activity

9:00

10:00

Welcome, Coffee, Donuts

10:00

11:00

Product & Services Review

11:00

12:00

Valuation Review (State of the Golden Goose)

12:00

12:30

Lunch (on-site)

12:30

13:00

Growth Potential (new products, services and business models)